Choose from 5 options:

AICIS undertakes pre- and post-market risk assessments/evaluations to identify potential risks to human health and/or the environment that may be associated with the import, manufacture, formulation, use, storage and disposal of industrial chemical(s) in Australia. AICIS makes recommendations to relevant risk management agencies, where required, to ensure appropriate controls are in place for the protection of human health and/or the environment from their introduction and use.

AICIS issues certificates and commercial evaluation authorisations for the introduction of unlisted industrial chemicals into Australia following a pre-market assessment. AICIS also monitors reported and exempted chemical introductions and maintains the Australian Inventory of Industrial Chemicals (The Inventory).

Assessment/evaluation statements are published on the AICIS website for use by all stakeholders, including other Australian Government and state and territory regulatory agencies such as public health, worker health and safety, environmental, transport and consumer product safety agencies.

AICIS implements a science strategy to maintain high quality scientific risk assessments though delivery of various technical outputs such as technical training and guidelines, gathering chemical intelligence, and collaborating with other chemical regulatory authorities to inform assessment and evaluation activities.

AICIS also assists Australia to meet its obligations under international agreements regarding industrial chemicals and works with other countries to harmonise and adopt (where applicable in the Australian context) international standards and risk assessments methods

AICIS undertakes activities such as compliance monitoring of introducers of industrial chemicals under the Industrial Chemicals Act 2019, compliance audits, managing compliance cases, liaising with other Australian enforcement agencies and administering Australia's obligations relating to industrial chemicals under the Rotterdam and Minamata Conventions.

The Industrial Chemicals Categorisation Guidelines and the Industrial Chemicals (Fees and Charges) Rules, are regularly reviewed and updated to ensure AICIS regulation remains contemporary and fit for purpose. AICIS also provides stakeholder education and guidance on the industrial chemicals legislative framework to assist Industry understand their regulatory obligations.

Corporate activities support the efficient and effective administration of the Scheme. These include: managing the Industrial Chemicals Special Account and cost recovery arrangements, registration of introducers and maintenance of the Register of Industrial Chemical Introducers, strategic communication and website management, stakeholder engagement, and ensuring the Scheme’s compliance with regulatory and business reporting requirements.

The cost base for AICIS comprises several activities which, when taken together, are necessary to efficiently and effectively regulate the introduction of industrial chemicals under the Industrial Chemicals Act 2019. These activities can be aggregated and grouped into two broad categories: regulatory outputs and support activities.

Regulatory outputs are activities provided to an individual or organisation or those provided to a broader group of individuals and organisations. In 2023-24, AICIS will continue to recover the costs of undertaking regulatory activities using a combination of fees and charges (levies) based on the demand for a government activity or intervention.

AICIS charges fees for services where a direct relationship exists between the regulatory activity and the individual or organisation requesting that specific activity. All regulated entities are charged the same fee for the same activity. Under these circumstances, the activities performed, and their associated costs are driven by a specific need and demand created by the applicant (an application).

Each fee for service item can be broken down into a number of business processes. For all applications, the business processes are:

When the cost of the AICIS activity can be reasonably attributed to a broader group of organisations (or individuals) rather than a single entity, the activity will continue to be funded through a cost recovery levy. In these instances, the level of demand for Government activity or intervention is collectively driven by the industry as a whole rather than a single entity within it. Table 1 outlines regulatory outputs and support activities classified as direct costs and support activities that are classified as indirect costs.

Table 1 – Examples of AICIS outputs as direct and indirect costs

| Regulatory outputs: Direct costs (fees for services) | Regulatory outputs: Direct costs (cost recovery levies) | Support activities: Indirect costs |

|---|---|---|

| Registration of introducers | Compliance monitoring and enforcement | Management of Special Account |

| Certificate applications | Post-market evaluation of chemicals | Human resources management |

| Authorisation applications | Pre-introduction reports and post-introduction declarations | Corporate governance |

| Inventory listing applications | Maintenance of Inventory | Facilities and building |

| Confidential business information (CBI) protection applications | Stakeholder engagement/education | Website and IT |

| Applications for import / export of industrial chemicals into or out of Australia | Enquiries and complaints management | Regulatory and business reporting |

The key cost drivers in estimating the cost base for AICIS are:

When AICIS was established in 2020-21, regulatory charging was based on historical effort data (resources required and frequency or annual volume data) from comparable NICNAS activities (where available). These activities were used as a proxy to estimate the effort and corresponding cost of undertaking similar AICIS activities. Where comparable NICNAS activities were not identified, management estimates were used for effort and corresponding costs. It has since been identified that fundamental differences between the schemes limits the utility of historical data as a wholly reliable proxy of true effort and associated costs for all regulatory activities. Estimates of volumes were affected by impacts of the COVID-19 pandemic on global supply chains and domestic markets.

To refine effort and cost estimates, historical data have been used to establish a resource baseline that is adjusted as actual scheme data become available. This has allowed AICIS to better understand the efficient resourcing requirements for administering the scheme (see ‘Ongoing commitment to appropriate charging arrangements’ below).

Additionally, an in-depth time capture exercise has been undertaken to validate effort estimates used to date and identify potential changes to future charging arrangements; initially conducted over 11 weeks between October and December 2021. Due to a lack of volumes across specific activities, a supplementary time capture exercise commenced in September 2022 and is ongoing.

Collected data indicates more effort was spent on some fee for service activities than historically estimated. As AICIS application volumes are yet to normalise and the effort observed across similar activities has been variable, AICIS considers that it would not be appropriate to adjust fees for services at this stage. To further refine the accuracy and robustness of effort estimates in the Activity-Based Costing model, the time capture exercise will continue. Any proposed changes will be the subject of consultation with industry stakeholders in the context of development of the 2024-25 CRIS.

The cost of the environmental component of risk assessments undertaken by DCCEEW are included within the AICIS cost base. Table 2 details the estimated cost base for the 2023-24 financial year and forward estimates for the following three years.

Table 2 - AICIS estimated cost base, 2023-24 to 2026-27 ($’000)

| Expenses | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|

| Employee and contractor expenditure | 13,360 | 13,757 | 14,166 | 14,587 |

| Non-employee expenses | ||||

| Supplier (including DCCEEW) | 7,148 | 7,302 | 7,410 | 7,521 |

| Depreciation3 | 1,120 | 1,120 | 1,120 | 1,120 |

| Allocation to operating reserve4 | - | - | - | - |

| Total5 | 21,628 | 22,179 | 22,696 | 23,227 |

The cost base in its entirety comprises the estimated costs of efficiently and effectively delivering regulatory functions. Costs such as those incurred for policy functions by other areas within the Department of Health and Aged Care, other than AICIS, are specifically excluded from the cost base, as these are funded by Government.

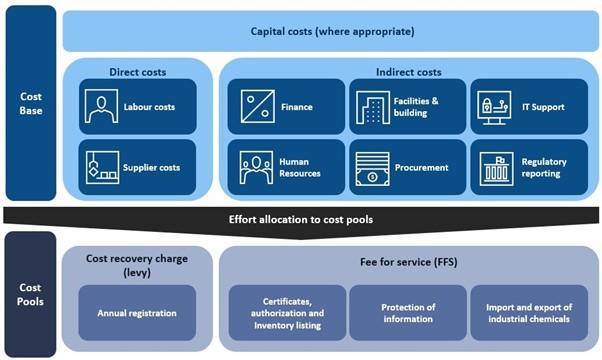

AICIS uses an activity based costing (ABC) methodology to allocate all direct and indirect costs incurred by AICIS and DCCEEW to each activity and subsequently each charge point.

The cost base comprises:

Figure 1 (below) presents a schematic of the activity based cost model. An example of how a fee for service item is calculated is included at Attachment A.

Figure 1 – Activity Based Cost Model

Table 3 shows the estimated total cost of regulatory activities inclusive of support function costs using the ABC methodology.

Table 3 - Estimated cost by regulatory output for 2023-24 ($’000)

| Regulatory activities | Fee or Levy | Cost ($’000) |

|---|---|---|

| Registration applications | Fees for service | 561 |

| Certificate applications | Fees for service | 737 |

| Commercial evaluation authorisation (CEA) applications | Fees for service | 29 |

| Inventory Listing applications | Fees for service | 9 |

| Confidential business information (CBI) protection applications | Fees for service | 630 |

| Import / export of industrial chemicals into or out of Australia applications | Fees for service | 0 |

| Compliance monitoring and enforcement | Levy | 5,163 |

| Post-market evaluation of chemicals | Levy | 12,213 |

| Pre-introduction reports | Levy | 213 |

| Specific Information Requirements | Levy | 530 |

| Post-introduction declarations | Levy | 308 |

| Maintenance of Inventory | Levy | 1,161 |

| Stakeholder engagement/education | Levy | 261 |

| Enquiries and complaints management | Levy | 320 |

| Total6 | 21,568 | |

Figures include direct and indirect costs. Figures may not total due to rounding.

AICIS’s approach to activity based costing seeks to confirm the level of effort spent against a regulatory activity is proportionate to the risk. Fees for services have been maintained at 2022-23 rates while further effort data is collected to determine the true efficient cost of providing each service.

The Charging Framework state that the levy payable should bear a reasonable relationship to the driver of regulatory activities in a manner that approximates the level of resources required to provide the activity across the regulated group.

As demonstrated in Table 3 above, the evaluations program and compliance program are the two biggest regulatory outputs intended to be recovered through the cost recovery levy. The information provided below demonstrates the link between risk and regulatory effort for these key regulatory outputs. This reflects the post-market nature of the scheme’s design.

AICIS evaluates risks from industrial chemicals already authorised for introduction and use in Australia, predominantly chemicals already listed on the Inventory. AICIS can also evaluate chemicals that are introduced under an assessed certificate or the reported or exempted categories, in response to emerging concerns and/or new information. In consultation with stakeholders, AICIS has committed to identify and prioritise industrial chemicals currently in use for evaluation that do not have a current risk assessment using the Evaluations Prioritisation Tool (EPT) and Evaluation Selection Analysis (ESA) criteria and process.

Limited available data suggests that as annual introduction value increases, businesses generally introduce:

AICIS uses a risk-based approach to promote awareness of obligations, check record-keeping requirements and identify and manage cases of non-compliance. By modifying monitoring activities to accommodate emerging risks, AICIS focuses on introducers at higher risk of non-compliance and introductions that pose a higher risk to human health and the environment. It is not possible to ascertain every introducer’s degree of compliance in advance of undertaking compliance monitoring or to base the funding model on the degree of risk of the chemicals introduced.

In monitoring compliance, when there are no other risk indicators – for example, among a group of industrial chemical introducers with no prior compliance history – regulatory effort is prioritised using introduction value as a proxy for exposure (and therefore risk). This is because, in a group of introducers introducing similar products, those introducing a greater introduction value will be importing/manufacturing a greater volume, which will result in greater risk and therefore, proportionately, greater regulatory effort.

To develop a charging regime that aligns with the Charging Framework, the most appropriate method for funding regulatory activities through the registration levy must be determined. The central principle of the Charging Framework is that charging be aligned with the drivers of regulatory effort.

The risk posed by a chemical is a function of hazard and exposure; exposure is a function of use pattern and volume. As the hazard of a chemical cannot be changed, risk management involves minimising exposure, where required. The risk-based approach for funding regulatory activities that are not services provided to identifiable recipients is also primarily based on levels of exposure of humans and the environment.

It is a long established international practice for the annual volume of introduced chemicals to function as a proxy for exposure, as a larger volume generally translates into more workers exposed, or more consumer products on the shelves (public exposure), or more of the chemical flowing down drains and into waterways (environmental exposure).

However, AICIS does not hold nor have legal authority to obtain data on the volumes of all industrial chemicals introduced into Australia. Furthermore, obtaining such data would involve substantial additional regulatory burden on industry, which is contrary to the policy aims of the recent reforms.

The value of introductions is readily available to Government, at the least burden to industry. As established above, introduction value is closely correlated with introduction volume and an increase in the number and complexity of chemicals introduced, which is indicative of risk that requires proportionate regulatory effort. It is on this basis that introduction value has been the legislative basis on which the levy was established under the former NICNAS for over 25 years and continues to apply under AICIS.

At this stage, there are insufficient data to definitively determine whether introduction value is the most appropriate proxy for regulatory effort. Through the effort data capture process undertaken by AICIS and DCEEWW, the data set will be more robust and analysis of a more robust data set will determine whether alternative charging approaches are more suitable to better align costs with charges. Any proposed changes will be included in the 2024-25 CRIS. Stakeholder consultation will occur before any proposed charging approaches are implemented.

The introduction value thresholds for charging the registration levy are aligned with the risk-based approach to determining regulatory effort outlined above. Lower value introducers generally introduce lower volumes of chemicals resulting in lower human and environmental exposures than higher value introducers. However, at the higher value of introductions, the regulatory effort required does reach a plateau at a point, so it would not be risk-proportionate to charge a higher registration levy once the plateau has been reached.

AICIS will continue to monitor the maturation of the scheme to a steady state given it is a relatively new scheme. This will help AICIS to refine effort drivers for both levy funded and fee for service activities and thus ensure that fees and charges reflect the efficient cost of delivering regulatory activities and services. AICIS will also consider how to appropriately address the accumulation of prior year revenue held in the Industrial Chemicals Special Account. These issues will be further considered in consultation with Industry.

A moderate increase in fee for service application volumes is predicted for 2023-24, however a steady state for these applications has not yet become apparent under AICIS. In addition, higher than estimated effort to process certain application categories has been observed over the first three years of the scheme, due to some applications containing more supporting data than expected. Efforts to streamline assessment processes are underway.

Given the uncertainty outlined above, the need to gather more effort data, and to avoid undue price volatility for industry, fees for services in 2023-24 are proposed to be maintained at their 2022-23 rates. Further effort data will be collected in 2023-24 and fees recalibrated where appropriate in 2024-25.

Conversely, levy prices will be further reduced across all registration levels by approximately 11.7%. This reduction responds to consecutive operating budget surpluses resulting from higher than anticipated number of registrants at the higher registration levels, and the substantial increase in the interest equivalency payment on the special account expected for 2023-24 from $34k to $758k. This aligns with the balance management in strategy (refer to Section 4) of aligning revenue and expense to result in a break-even forecast for 2023-24.

3 Depreciation expenses are based on the existing asset profile, subject to change if assets are acquired or fully depreciated.

4 An operating reserve is maintained in accordance with the Balance Management Strategy at Section 4.

5 The total estimated cost base includes the cost of activities considered non-recoverable under the Charging Framework. These costs will not be recovered through the proposed fees and charges as indicated in Table 3.

6 Total estimated cost by regulatory output for 2023-24 excludes the FOI/non-cost recoverable amount of approximately $60k